The long term strategy of the EU is to become climate neutral by 2050 by transitioning its economy to become net zero in greenhouse gas (GHG) emissions. As such, the Commission proposed the 2030 Climate Target Plan to raise the EU’s ambition on reducing GHG emissions to at least 55% below 1990 levels by 2030. As a result, the Flemish government rolled out the Flemish Energy and Climate plan for 2021-2030 to reduce GHG emissions in non-Emissions Trading Scheme sectors (ETS) by 40%. To gain further insight into the needs and expectations of entrepreneurs regarding the main technical and economic preconditions to make their climate plans possible, VLAIO is requesting a summary of an enterprise’s Climate Plan. This will come into effect as of the 1st of October 2022.

What is the Climate Plan?

The Climate Plan describes how a specific Flemish site of a company will transition towards low-carbon operations in a climate-neutral Europe by 2050, taking into account the objectives of the Flemish Energy and Climate Plan (Horizon 2030). VLAIO has now installed the admissibility requirement to submit a summary of a company’s Climate Plan for many Flemish programmes such as:

- Research and development projects

- Feasibility studies

- Baekeland mandates

- Innovation mandates (phase 2)

- Partnerships in ICON projects

- Partnerships for projects in the framework of a spearhead cluster

Who falls under scope?

For projects submitted from 1 October 2022 onwards, an explanation of the company’s climate plan must be enclosed with the aid application if the (co-)applicant is

- a large company

According to the European definition, small-to-medium sized enterprises (SMEs) have less than 250 employees and either an annual turnover of no more than € 50M or a balance sheet total of no more than € 43M. In certain cases, the data of other companies must also be included for the calculation of the SME criteria mentioned above. (“consolidation of the accounts”). This is the case when the enterprise is not an independent enterprise. In general, a business loses its independence when there is (or more) a “partner enterprise” ( >= 25% of the capital or voting rights) or “linked enterprise” ( > 50% of the capital or voting rights). - an energy-intensive enterprise

Company with a final energy consumption of more than 0.1 PJ (petajoule) at the branch level (0.1 PJ = 27.8 GWh of electricity, gas, fuel, …). This involves looking at the location in Flanders where most of the valorisation of the requested support will take place.

For the Strategic Transformation Support (STS) programme, SMEs should also provide a climate plan, albeit the plan is subjected to other criteria.

Format of the Climate plan

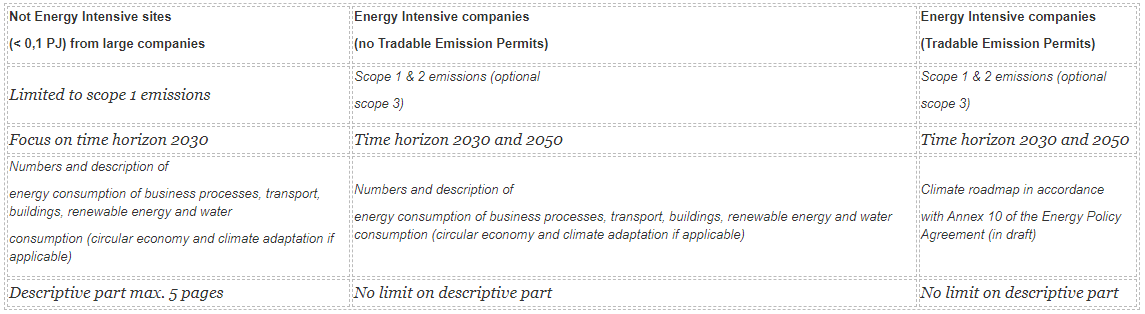

In general, the climate plan should be an explanatory document on how a company is approaching the energy transition. In this respect, it should include the key steps that it will take to reduce or prevent their GHG emissions. However, the content of the Climate Plan may vary for companies under ETS or if they are considered as energy-intensive. Based on this, the company should report on their emissions. There are three main categories or scopes of emissions:

- Scope 1: it covers direct emissions, from sources that a company owns or directly controls (e.g., emissions associated with fuel combustion in boilers, furnaces, vehicles).;

- Scope 2: this scope covers indirect GHG emissions associated with the purchase of electricity. Although scope 2 emissions physically occur at the facility where they are generated, they are accounted for in an organisation’s GHG inventory because they are a result of the organisation’s energy use;

- Scope 3: emissions that are not produced by the company itself, and not the result of its own activities from assets, but by those that it’s indirectly responsible for, up and down its value chain.

In the table below, an overview on the content of Climate Plan is presented per company type.

When is a Climate Plan not required?

A resubmission of the Climate Plan is not required if VLAIO already approved a Climate Plan that is less than 4 years old, or if an ETS company already had to submit a climate roadmap in the framework of the Energy Policy Agreement (EPA) / EnergieBeleidsOvereenkomst (EBO).

Transition period

For funding applications, submitted until the end of the year (2022), VLAIO installed a transition period. In this case, VLAIO allows companies to submit their projects on the 1st of January 2023 latest.

For energy-intensive companies that are planning to join the EPA for the period 2023-2026, the deadline to submit a Climate Plan is extended to 31 December 2024.

To find out more on this topic and on how we can assist you, please reach out to Tom Wallyn, Guillaume Goeders, or Bart Wyns of the PwC Incentives Hub.